Delaware franchise tax is the mandatory annual fee all domestic corporations, LLCs, limited partnerships, and general partnerships must pay to maintain good standing in the state. This fee is not an income tax. It is a charter maintenance fee owed regardless of whether your business earned a dollar or sat completely dormant. The Delaware Division of Corporations administers the tax, sets fixed deadlines, and enforces penalties for late payment. Business owners who understand the two calculation methods and key due dates can avoid overpaying by thousands of dollars each year.

What are the Delaware franchise tax calculation methods?

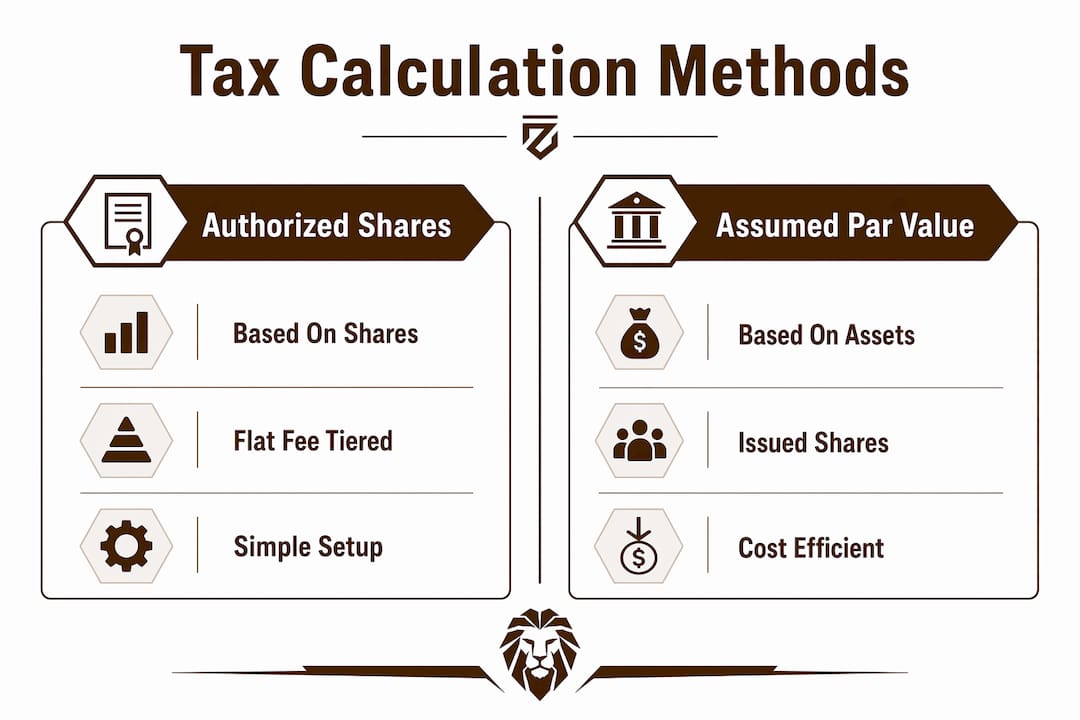

Delaware corporations have two calculation methods available, and choosing the wrong one is the most expensive mistake a business owner can make.

Authorized Shares Method

The Authorized Shares Method calculates tax based on the total number of shares a corporation has authorized, not the shares actually issued. The minimum tax under this method is $175, and the maximum is $200,000. Delaware's online portal defaults to this method. That default is a serious problem for startups, which typically authorize millions of shares at incorporation to allow for future fundraising. A corporation with 10 million authorized shares can receive a tax bill exceeding $75,000 under this method, even if it has no revenue and minimal assets.

Assumed Par Value Capital Method

The Assumed Par Value Capital Method calculates tax based on total gross assets and issued shares. For most early-stage companies, this method produces a dramatically lower tax bill. The minimum tax under this method is $400, and the maximum remains $200,000. To use it, you must supply your total gross assets and the number of shares actually issued when filing. If you omit that data, Delaware automatically applies the Authorized Shares Method and bills you accordingly.

Pro Tip: Always enter your total gross assets and issued shares during filing. Leaving those fields blank triggers the Authorized Shares Method by default, and the resulting bill can be 10 to 100 times higher than necessary.

| Feature | Authorized Shares Method | Assumed Par Value Capital Method |

|---|---|---|

| Basis of calculation | Total authorized shares | Total gross assets and issued shares |

| Minimum tax | $175 | $400 |

| Maximum tax | $200,000 | $200,000 |

| Best for | Corporations with few authorized shares | Startups with many authorized but few issued shares |

| Portal default | Yes | No. Must input asset and share data manually |

The $50 annual report fee applies to both methods and is required alongside the tax payment for domestic corporations.

When are Delaware franchise tax payments due?

Deadlines differ by entity type, and missing them triggers immediate financial penalties.

Domestic corporations face the strictest timeline. Every domestic Delaware corporation must file an annual report and pay franchise tax by march 1 each year. That deadline is absolute. Delaware does not shift the march 1 due date if it falls on a weekend or holiday. The filing and payment must arrive on that exact date regardless of the calendar.

LLCs, limited partnerships, and general partnerships operate on a different schedule. These entities pay a flat annual tax of $300 due june 1 each year. No annual report is required for these entity types. The flat fee structure makes compliance simpler, but the june 1 deadline is equally firm.

Quarterly estimated payments for large tax liabilities

Corporations expecting to owe $5,000 or more in franchise tax must follow a quarterly estimated payment schedule. The structure is:

- 40% of estimated tax due june 1

- 20% of estimated tax due september 1

- 20% of estimated tax due december 1

- Remaining balance due march 1 of the following year

This schedule applies to the current tax year's estimated liability. Corporations that underestimate and miss quarterly targets can face additional interest on the shortfall. Planning your estimated payments against prior-year tax data is the most reliable way to stay on track.

Key points to keep in mind for all entity types:

- The march 1 and june 1 deadlines apply to the prior calendar year's tax obligation.

- No extensions are available for either deadline.

- Quarterly payments apply only to corporations with an estimated liability of $5,000 or more.

- LLCs and partnerships have no quarterly payment requirement.

What are the penalties for late Delaware franchise tax payments?

Missing a franchise tax deadline costs money immediately. A $200 late filing penalty applies the moment the march 1 deadline passes without payment. On top of that, Delaware charges 1.5% monthly interest on any unpaid tax balance until the full amount is paid. That interest compounds every month, so a delayed payment of $5,000 adds $75 in interest charges in the first month alone, and the total grows from there.

The financial penalties are only part of the problem. Late or missed payments cause your entity to lose good standing with the state. Loss of good standing has real operational consequences:

- Banks and lenders routinely require a Certificate of Good Standing before approving business loans or credit lines.

- Investors and acquirers check good standing status during due diligence. A lapsed status can delay or kill a funding round.

- Contracts and government licenses in many states require proof of good standing from your state of incorporation.

- Reinstating good standing after a lapse requires paying all back taxes, penalties, and interest in full before the state processes reinstatement.

One detail many business owners miss: simply ceasing operations does not stop franchise tax obligations. The tax accrues every year as long as the entity exists in Delaware's records. A dormant company that stopped doing business five years ago still owes five years of franchise tax, penalties, and interest. The only way to stop the obligation is formal dissolution, with all back taxes and reports current at the time of filing.

How to file Delaware franchise tax online

The Delaware Division of Corporations provides an online portal for franchise tax filing and payment. The process is direct, but having the right data ready before you start prevents errors.

- Gather your required documents. You need your Delaware Entity File Number, total gross assets from your most recent balance sheet, total number of authorized shares, and total number of issued shares.

- Access the Division of Corporations portal. Go to the Delaware Division of Corporations website and select the franchise tax filing option for your entity type.

- Select your calculation method. For corporations, you will see the Authorized Shares Method pre-selected. Enter your total gross assets and issued shares to switch to the Assumed Par Value Capital Method and see the lower calculated amount.

- Complete the annual report. Corporations must file the annual report at the same time as the tax payment. The report requires officer and director information, registered agent details, and principal business address.

- Pay the tax and filing fee. Delaware accepts credit card and electronic check payments. The $50 annual report fee is added automatically for corporations. Confirm the total before submitting.

- Save your confirmation. Download or print the payment confirmation immediately. Store it with your corporate records for at least seven years.

Pro Tip: Pull your balance sheet total gross assets figure from the same fiscal year end that corresponds to the tax year you are filing. Using the wrong year's asset figure is a common error that can invalidate your Assumed Par Value calculation and trigger a reassessment.

The entire filing process takes under 30 minutes when your documents are ready. The most time-consuming step is locating the correct gross asset figure if your accounting records are not organized.

Key Takeaways

Delaware franchise tax is a mandatory annual fee, not an income tax, and choosing the Assumed Par Value Capital Method is the single most effective way for most corporations to reduce their tax liability.

| Point | Details |

|---|---|

| Tax is not income-based | Franchise tax is owed regardless of revenue, profit, or business activity. |

| Method selection matters | The Assumed Par Value Capital Method typically produces a far lower bill than the default Authorized Shares Method. |

| Deadlines are fixed | Corporations must file and pay by march 1; LLCs and partnerships by june 1, with no extensions. |

| Penalties start immediately | A $200 penalty plus 1.5% monthly interest applies the day after the missed deadline. |

| Dissolution stops the obligation | Formally dissolving the entity is the only way to end annual franchise tax liability. |

Why I tell every founder to check their calculation method first

Founders consistently underestimate how much the default calculation method costs them. I have seen early-stage companies with 10 million authorized shares receive initial tax notices above $50,000, when their actual liability under the Assumed Par Value Capital Method was $400. That gap is not a rounding error. It is the difference between a manageable compliance cost and a cash crisis for a pre-revenue startup.

The fix is simple, but only if you know to look for it. Delaware's portal does not explain the two methods or prompt you to choose. It just shows you a number based on your authorized shares and waits for payment. Most founders pay it without question, assuming the state calculated correctly. The state did calculate correctly. It just used the method that produces the highest possible bill.

Quarterly estimated payments are another area where I see businesses get caught off guard. If your franchise tax liability crosses $5,000, you owe payments in june, september, and december, not just at year end. Missing those quarterly installments does not trigger the $200 flat penalty, but it does generate interest charges that add up over the year. Track your estimated liability against prior-year actuals and set calendar reminders for each quarterly date.

One more point that does not get enough attention: if you are winding down a Delaware entity, file for formal dissolution before the next march 1 deadline. Owners who simply stop operating and ignore the annual filings accumulate years of back taxes, penalties, and interest. By the time they try to close the entity properly, the reinstatement cost can exceed the original tax liability many times over. Formal dissolution is the clean exit. Everything else is just deferred debt.

— Joshua

Zeuzcompliance and Delaware compliance filing

Managing Delaware franchise tax obligations across multiple entities or jurisdictions adds real administrative load to any business operation. Missed deadlines, wrong calculation methods, and incomplete annual reports each carry financial consequences that compound over time.

Zeuzcompliance provides automated deadline tracking, calculation support, and filing guidance for Delaware franchise tax and annual report requirements. The platform covers multi-jurisdictional compliance across the US, UK, Australia, New Zealand, and Europe, so business owners manage all obligations from a single dashboard. Real-time alerts flag upcoming due dates before penalties apply. Accurate calculation workflows reduce the risk of defaulting to the Authorized Shares Method. Filing records are stored and accessible for audit purposes. Zeuzcompliance replaces manual tracking with automated workflows built for businesses that cannot afford compliance errors.

FAQ

What is Delaware franchise tax?

Delaware franchise tax is an annual fee charged to corporations, LLCs, limited partnerships, and general partnerships incorporated or registered in Delaware. It is a charter maintenance fee, not an income tax, and is owed regardless of business activity or profit.

What is the Delaware franchise tax due date for corporations?

Domestic corporations must file their annual report and pay franchise tax by march 1 each year. Delaware does not extend this deadline if it falls on a weekend or holiday.

How do I calculate Delaware franchise tax using the Assumed Par Value Capital Method?

Enter your total gross assets and total issued shares in the Delaware Division of Corporations online portal. The system calculates your tax under the Assumed Par Value Capital Method, which typically produces a lower bill than the default Authorized Shares Method.

What happens if I miss the Delaware franchise tax deadline?

A $200 late penalty applies immediately, plus 1.5% monthly interest on the unpaid balance. Your entity also loses good standing, which can block loans, contracts, and investor transactions until all amounts are paid in full.

Do Delaware LLCs pay franchise tax?

Delaware LLCs pay a flat annual tax of $300 due june 1. No annual report is required. The flat fee applies regardless of the LLC's revenue or assets.